Exploiting Price Inefficiencies: Scaling Forex with Arbitrage Scanner V2

In the institutional trading landscape, the fastest execution networks don't predict where the market is going—they exploit microscopic valuation discrepancies that exist right now. For retail day traders working on ultra-low timeframes like the 1-minute (M1) chart, competing on pure direction can be a punishing experience due to retail spread widening and sudden liquidity dumps. To secure a resilient statistical edge, professional algorithmic traders pivot away from speculative technical models and focus instead on statistical arbitrage.

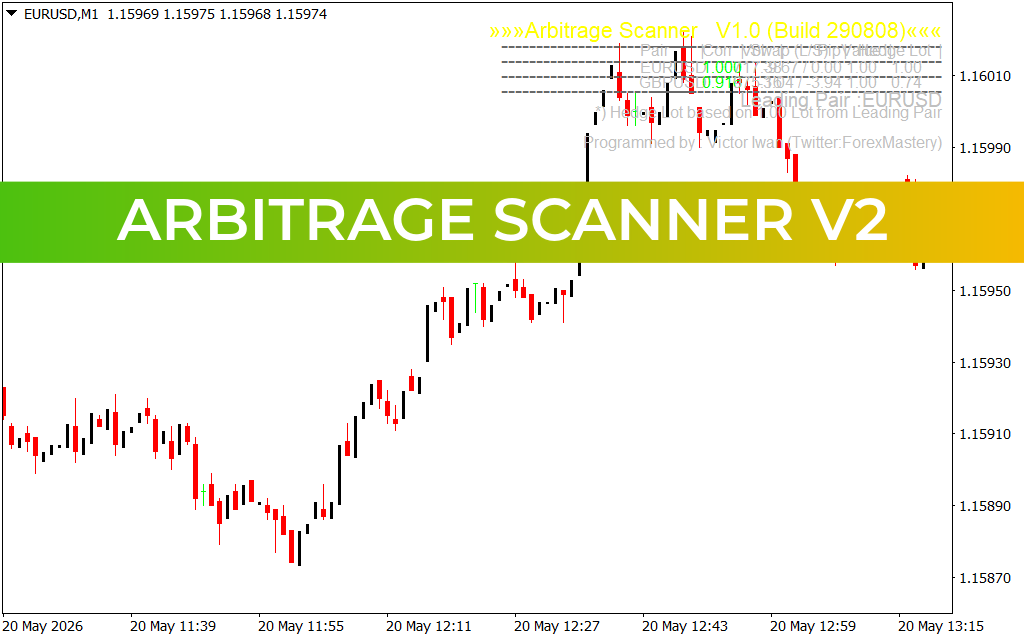

Looking closely at the EUR/USD M1 price delivery during the May 20th session, the market transitions through distinct structural imbalances. After forming a local accumulation floor beneath 1.15890, a dramatic influx of cross-currency volume hits the market at 11:55. This initiates a vertical markup phase, propelling the exchange rate aggressively through major psychological layers to peak near 1.16010. During such high-velocity expansions, correlated financial instruments across separate brokers or underlying synthetic pairs frequently fall out of mathematical alignment for brief windows. Tracking and capturing these rapid pricing mismatches is exactly how the Arbitrage Scanner V2 software solidifies your marketplace edge.

The Architecture of Multi-Instrument Spread Trading

Unlike conventional lagging oscillators that track past price data, this advanced technical utility operates as a real-time correlation matrix directly on your primary workstation. It continuously monitors the price delivery of highly correlated assets (such as EUR/USD and GBP/USD) alongside their synthetic cross rates to detect mathematical divergence from true fair value.

When integrated into a fast-paced M1 workspace, the system delivers immediate structural advantages:

- Real-Time Spread Discrepancy Tracking: The indicator dashboard projects an on-screen statistical readout showing the precise correlation percentages and swap coefficients of leading currency pairs. If the leading pair surges while its core counterpart lags behind, the script highlights an active arbitrage corridor.

- Instantaneous Divergence Triggers: When the absolute price variance between the correlated assets exceeds an optimized historical threshold, the scanner flags an immediate execution setup. Traders can buy the undervalued asset and short the overvalued asset, locking in low-risk pips as the spread inevitably snaps back to its historical mean.

- Non-Directional Risk Mitigation: Because this approach capitalizes on the convergence of two separate instruments, your portfolio is shielded from broad macroeconomic shocks or erratic central bank spikes that typically wipe out standard directional stop losses.

Upgrading Platform Performance and Efficiency

Success in high-frequency arbitrage trading requires removing human latency and emotional hesitation. The Arbitrage Scanner V2 script handles complex computational matrix math directly inside your MetaTrader terminal, ensuring seamless background processing without inducing chart lag.

The fully customizable interface allows you to define target correlation coefficients, adjust lot allocation parameters based on account equity, and enable push or email alerts the exact moment a high-yield mispricing occurs. By anchoring your trading system to objective mathematical discrepancies rather than retail indicators, you protect your capital base and scale your intraday returns with institutional-grade precision.

2 Downloads

Last Update:

May 20, 2026 16:20 PM

Published:

Jan 18, 2026 17:34 PM

Category: